Featured

Table of Contents

Note, however, that this doesn't state anything about adjusting for inflation. On the bonus side, also if you think your option would certainly be to buy the securities market for those 7 years, which you 'd obtain a 10 percent yearly return (which is much from particular, particularly in the coming decade), this $8208 a year would certainly be more than 4 percent of the resulting small supply value.

Instance of a single-premium deferred annuity (with a 25-year deferment), with 4 payment alternatives. The monthly payment here is greatest for the "joint-life-only" option, at $1258 (164 percent greater than with the instant annuity).

The way you buy the annuity will identify the solution to that inquiry. If you acquire an annuity with pre-tax bucks, your premium lowers your taxable income for that year. According to , buying an annuity inside a Roth strategy results in tax-free payments.

What does a basic Fixed Indexed Annuities plan include?

The expert's initial step was to create a detailed monetary strategy for you, and afterwards describe (a) exactly how the suggested annuity suits your total strategy, (b) what alternatives s/he taken into consideration, and (c) exactly how such alternatives would or would not have actually resulted in lower or higher compensation for the consultant, and (d) why the annuity is the premium option for you. - Annuity accumulation phase

Naturally, an advisor may try pushing annuities also if they're not the best fit for your scenario and objectives. The factor can be as benign as it is the only product they offer, so they drop target to the typical, "If all you have in your tool kit is a hammer, pretty quickly whatever begins looking like a nail." While the consultant in this circumstance may not be unethical, it increases the risk that an annuity is a poor selection for you.

Lifetime Payout Annuities

Since annuities often pay the representative selling them much greater compensations than what s/he would get for investing your cash in common funds - Income protection annuities, let alone the absolutely no payments s/he would certainly obtain if you buy no-load mutual funds, there is a large motivation for representatives to press annuities, and the a lot more difficult the better ()

An underhanded expert recommends rolling that amount right into new "much better" funds that just happen to lug a 4 percent sales lots. Accept this, and the expert pockets $20,000 of your $500,000, and the funds aren't likely to perform better (unless you chose even much more inadequately to start with). In the same example, the consultant can steer you to buy a difficult annuity with that $500,000, one that pays him or her an 8 percent commission.

The consultant tries to rush your decision, claiming the offer will quickly vanish. It might undoubtedly, yet there will likely be equivalent deals later. The advisor hasn't figured out just how annuity payments will certainly be tired. The consultant hasn't revealed his/her payment and/or the charges you'll be charged and/or hasn't revealed you the effect of those on your ultimate repayments, and/or the settlement and/or charges are unacceptably high.

Current passion prices, and thus projected repayments, are historically low. Even if an annuity is best for you, do your due diligence in contrasting annuities marketed by brokers vs. no-load ones sold by the issuing company.

Is there a budget-friendly Retirement Annuities option?

The stream of month-to-month settlements from Social Protection is comparable to those of a delayed annuity. Since annuities are volunteer, the people getting them normally self-select as having a longer-than-average life expectancy.

Social Safety and security advantages are fully indexed to the CPI, while annuities either have no inflation protection or at the majority of use an established percent annual increase that may or might not make up for inflation in full. This kind of rider, just like anything else that increases the insurer's danger, requires you to pay more for the annuity, or approve lower settlements.

How do I apply for an Annuity Payout Options?

Disclaimer: This write-up is planned for informational objectives only, and ought to not be thought about financial recommendations. You need to consult a financial expert before making any significant economic choices.

Given that annuities are intended for retired life, taxes and charges might use. Principal Security of Fixed Annuities.

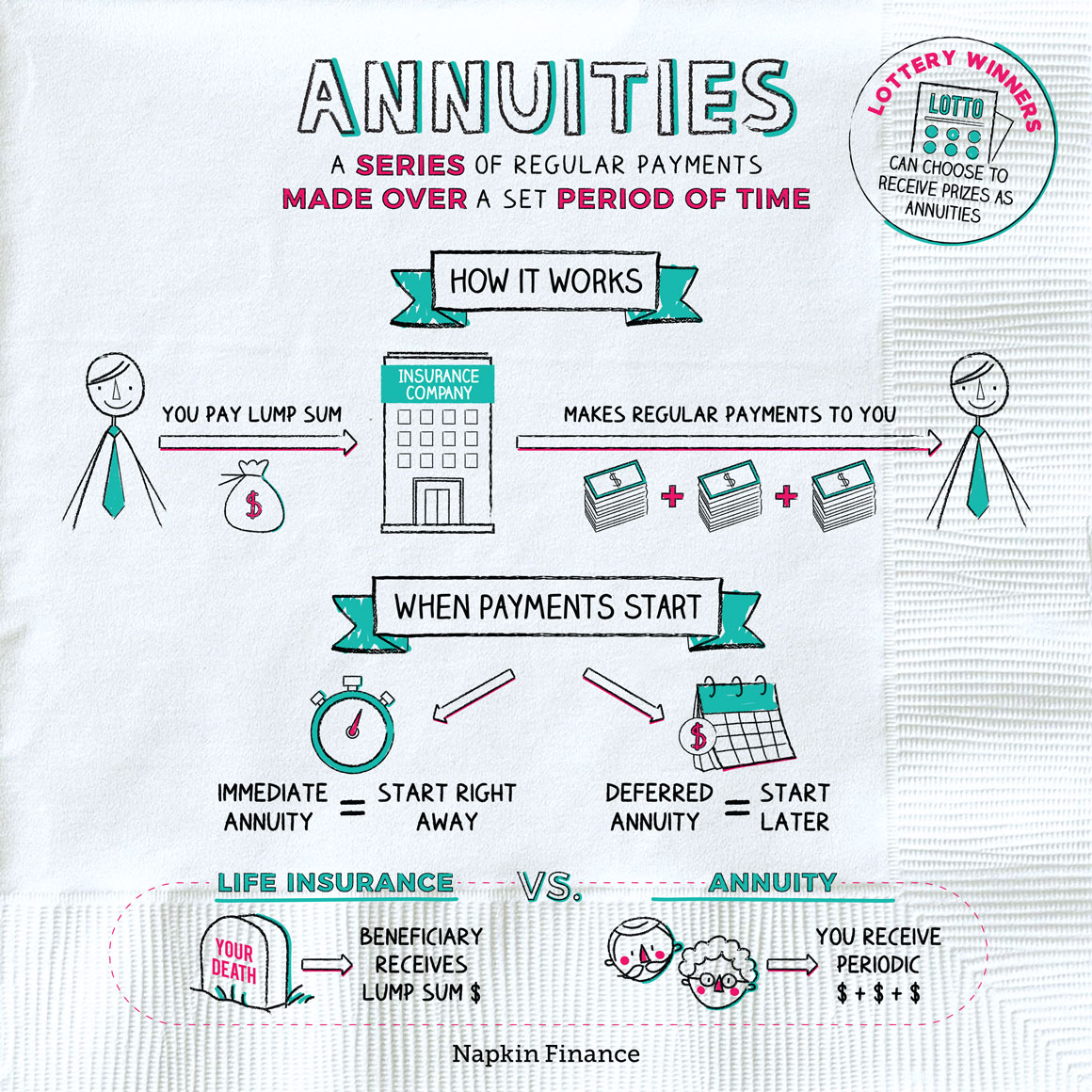

Immediate annuities. Deferred annuities: For those who want to grow their cash over time, yet are prepared to delay access to the money till retirement years.

Who has the best customer service for Guaranteed Return Annuities?

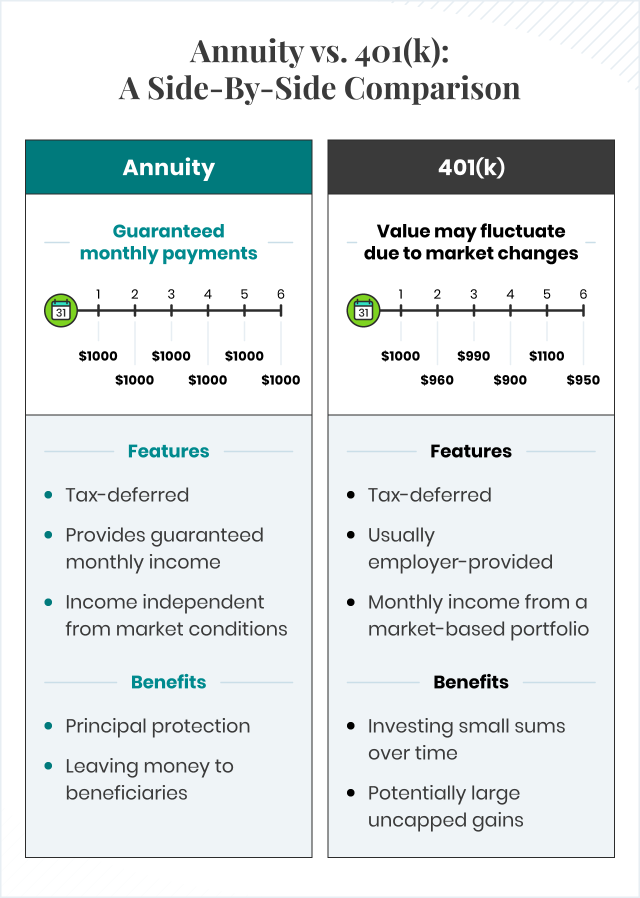

Variable annuities: Supplies better capacity for growth by investing your money in investment choices you pick and the ability to rebalance your profile based on your choices and in a method that aligns with altering economic objectives. With fixed annuities, the business spends the funds and gives a rate of interest to the client.

When a death case happens with an annuity, it is essential to have actually a named recipient in the agreement. Various choices exist for annuity death benefits, depending upon the contract and insurer. Selecting a reimbursement or "duration particular" choice in your annuity provides a survivor benefit if you die early.

Who offers flexible Retirement Income From Annuities policies?

Naming a recipient besides the estate can help this process go much more smoothly, and can help guarantee that the earnings go to whoever the private wanted the money to head to instead than going via probate. When present, a death advantage is immediately included with your contract. Relying on the kind of annuity you purchase, you might be able to include enhanced death benefits and functions, yet there can be additional prices or costs related to these add-ons.

{kind=link}

Table of Contents

Latest Posts

What types of Deferred Annuities are available?

What types of Tax-deferred Annuities are available?

What is the difference between an Fixed Indexed Annuities and other retirement accounts?

More

Latest Posts

What types of Deferred Annuities are available?

What types of Tax-deferred Annuities are available?

What is the difference between an Fixed Indexed Annuities and other retirement accounts?